- Used car market is tough but active

- E-PCP live retail values edge down

- Ex-fleet live retail values firm

THE July new car registration data shows the new car market has performed mildly better than the same month last year; volume is up 1.2%.

This is interesting given the time of year and specifically because general market feedback is that trading conditions have been difficult given both the weather and general economic concerns.

This means that the market as a whole is down 5.5% year to date – perhaps less than the industry expected – although the latter part of 2018 looks to be somewhat difficult from a demand and trading perspective. This will not have been helped by the increase in the Bank of England base rate either.

The diesel market has continued to suffer registration drops with a fall of 24.4% over the same period last year. Despite commitment to the fuel type from both the government and key manufacturers, consumers, whether fleet or private buyers, are still driven to petrol and hybrid vehicles for the time being.

The diesel market share for 2018 is down 11.2% year to date and rests at just 32.5% – a level few industry experts would have foreseen just a couple of years ago. This lower level of market penetration seems to have stabilised for the time being which is positive news for those planning future vehicle production and seeking to forecast future vehicle values.

For petrol powered cars the market has seen an increase in registrations of 20.1% over the same period last year and market share for the year to date is a substantial 61.8%.

Hybrid vehicle registrations have shown a lower improvement in volume than experienced in recent months at a still healthy 21% for the month, taking market share for the year to 5.7%. The volume of petrol cars being registered this year is likely to become an issue in future years as vehicles return to the used car market. Equally, there is wide speculation that pollution from petrol cars will increase notably and the industry is moving the issue from one fuel type to another.

Generally speaking, the July new car market has been a stable month when looking at registration data with a balance of buyers from both the private and fleet markets. There is no doubt there is some pent-up demand in the fleet sector due to the impending WLTP changes, and the August registration data will be very interesting.

Equally, the industry must be cognisant of the fact that “registrations” are not actually “sales” and the coming months are likely to be heavily influenced by commercial considerations and strategy in part brought on by legislative changes.

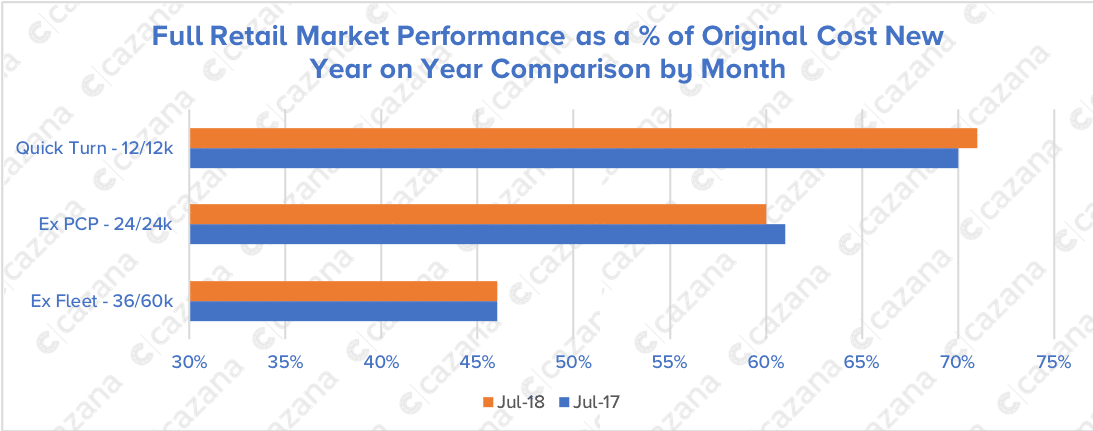

The used car market data collated by Cazana from live retail pricing has shown some interesting trends during 2018. With the industry-driven so heavily by the consumer these days, retail-driven insight has become ever more important. The next chart gives a high-level view of overall market performance at three key market profiles.

Data powered by cazana.com

Data collated during July shows that the quick turn sector of the market at one-year-old has in fact shown greater strength in retail pricing terms than it did in 2017. This shows that despite continued pre-registration activity the used car market is currently capable of absorbing younger low mileage cars. Naturally, there are a number of other types of used cars that fall into this category such as ex-manufacturer company vehicles and ex-rental cars, but with volumes of these low at this time of year there has not been pressure on values.

PCP cars continue to slide

For the second month running values of ex PCP profile cars have slipped. This is not due to a specific push on new car sales right now meaning a greater supply of these cars in the used market, it is more a reflection of the increased volumes of these registered two years ago. The focus is beginning to turn to what may happen when manufacturers do push sales in perhaps late August and certainly September and more of this profile of used stock does return to the used car market. It is fair to say that some pundits are seeing a potential issue as the year moves to the fourth quarter.

Fleet values consistent

Ex-fleet values have remained consistent in the market from a year on year comparison which is good news and a reflection of manageable volumes of cars during the month.

This stability is a trend for the year although it is of note that in comparison with June data there has been a two-percentage point drop in values and also a drop in the average cost new.

This could well be symptomatic of a reduction in overall volumes of fleet models returning to market due to apathy in the new fleet market. With real staple “non choice” business cars being churned as normal and users waiting to see the outcome of WLTP there may be some market volatility ahead in coming months.

The new diesel market seems to have found a level for itself for the time being which seems to be between twenty-five to thirty percent lower than last year in volume terms. In many cases despite continued damnation of diesel from a health and environmental perspective the used cars market remains robust. There is still a level of consumer misunderstanding on the forecourts, but fuel economy and running costs swiftly steer the retail buyer and for many diesel fuel is still a compulsive package when compared to petrol and hybrid vehicles unless annual mileage and travel patterns are low and local.

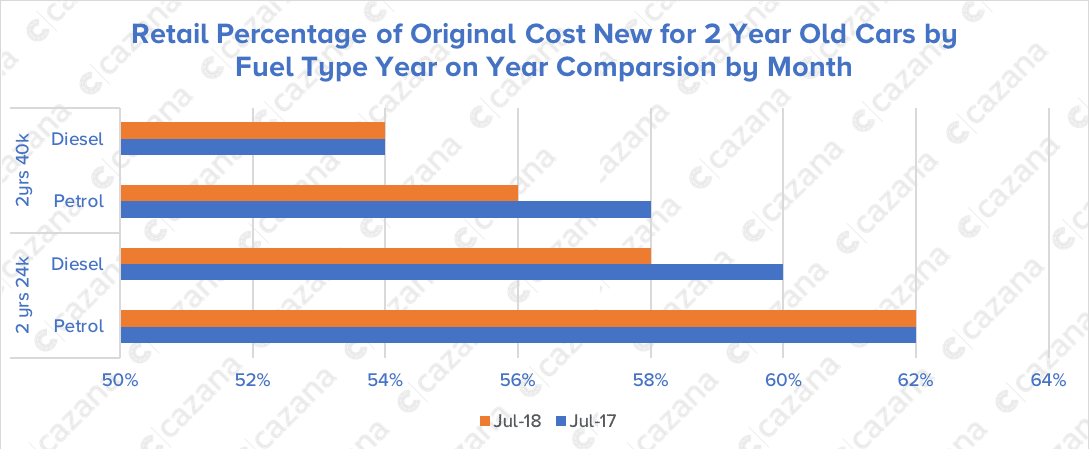

The next chart shows retail pricing performance of two-year-old cars by fuel type.

Data powered by cazana.com

This chart shows consistency in values year on year where the volume of product is freely available. It is not hard to find two-year-old ex fleet diesels with around 40k miles nor two-year-old petrol cars that are ex PCP with contracted mileage at around 24,000 miles. This picture may change as mentioned earlier as volumes increase later in the year.

The interesting point here is the drop-in retail pricing for the two-year-old petrol car with 40,000 miles and the two-year-old diesel with 24,000 miles. This may be due to changes in volume in the market although it is worth noting that whilst the average cost new for the petrol variants has remained similar the diesel average cost new has increased notably. This type of data needs more detailed investigation to reveal the root cause but it’s perhaps a noteworthy trend.

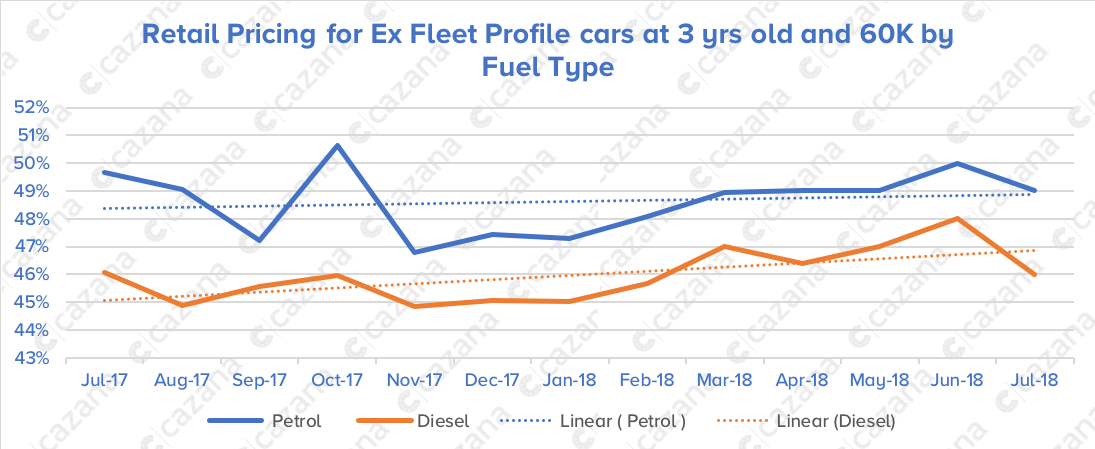

With the new fleet market currently running a little cool and new car demand anecdotally building in the background as a result of the WLTP confusion, the chart below shows the performance of the fleet sector in the used car market

Data powered by cazana.com

This chart shows that both petrol and diesel variants have been following a similar pattern in retail pricing terms. This is good factual data that shows the demand for diesel is consistent with petrol. This also shows that in comparison to July 2017 the value of a petrol car has dropped 1 percentage point to 49% of original cost new.

Diesel cars show consistency at 46% of cost new. There will undoubtedly be winners and losers in this detail of this data but clarity on the position of diesel demand in the new market is of significant importance.

July used market volatile

In summary, the July used car market has been more volatile than in previous months and given the fabulous weather that is understandable.

There are buyers but they need to be worked a little harder to get the final deal done. There is evidence of a drop-in retail pricing, indeed action in the wholesale market has generally been good. At the moment the impact of the latest interest rate increase is not clear, but it is likely to damage consumer confidence and affect spending especially amidst talk of a no Brexit deal economy next year.

Cazana’s realtime retail-based data is unique in providing up to the day market insight and intelligence being driven from over 16,000 websites each day. Seeking more focused information relating to specific market sectors or time periods ensures maximum vision and the most comprehensive insight required to maximise profit, ROI and asset management. This is exactly the data and insight required to deal with what will become a more challenging market later this year and further into 2019 and beyond.